Blog > Tougher Week for Rates - But Mortgage Applications Hit a 3-Year High

Tougher Week for Rates -But Mortgage Applications Just Hit a 3-Year High

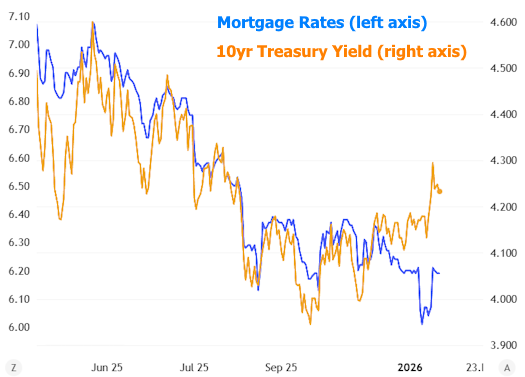

This week was a bit of a “two-steps-forward, one-step-back” moment for mortgage rates. We saw rates pull slightly higher early in the week, then calm down as markets settled. The bigger story (and the good news): mortgage demand surged — including purchase applications rising to their highest level in about three years.

This Week’s National Rate Snapshot

These are national averages (not a quote). Your exact rate depends on credit, down payment, occupancy, loan size, and more.

| 30-Year Fixed | 6.19% |

| 15-Year Fixed | 5.76% |

| 30-Year FHA | 5.85% |

| 30-Year Jumbo | 6.38% |

| 7/6 SOFR ARM | 5.71% |

| 30-Year VA | 5.87% |

Why Rates Felt “Stickier” This Week

Mortgage rates followed bond market volatility early in the week, driven by a mix of overseas bond selling and geopolitical headlines. The most important takeaway is that mortgage rates have been holding up better than Treasuries recently — meaning they’ve had a bit more insulation against jumping higher.

- Overseas bond volatility pushed global yields up temporarily.

- Geopolitical headlines added fuel early in the week before markets calmed.

- Mortgage-backed securities support has helped mortgage pricing outperform Treasuries recently.

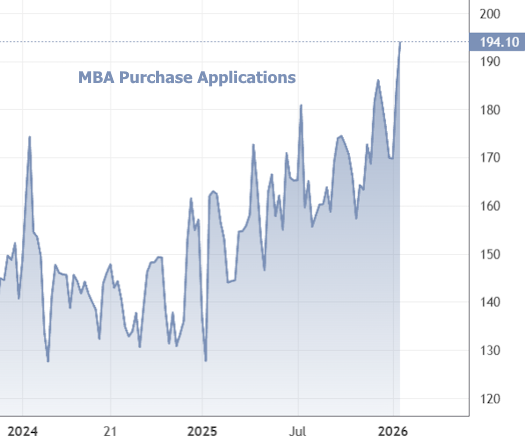

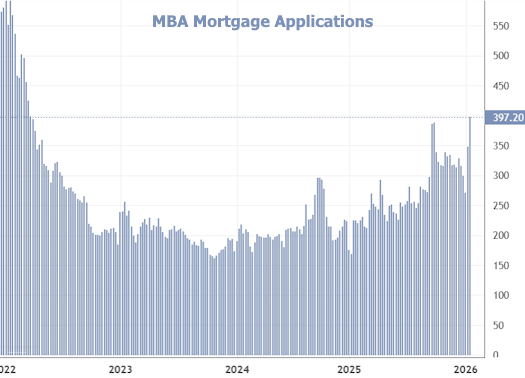

Mortgage Applications Just Spiked (Big)

Even with a tougher start to the week for rates, the Mortgage Bankers Association data showed a big jump in activity: refinance applications surged (which is typical after a strong rate rally), and purchase applications climbed to the highest level in about three years.

What This Means in Temecula (and Surrounding Areas)

For Temecula Valley buyers and homeowners, weeks like this usually create two opportunities:

- Buyers: If you’ve been waiting for a better window, improved demand can be a sign that other buyers are jumping back in. The right strategy matters (rate, payment, and offer terms).

- Homeowners: If you’re considering a refinance, VA IRRRL, or tapping equity, this is the kind of environment where it’s worth running numbers — even if we’re only slightly better than last week.

I’ll help you compare options (rate vs. fees, temporary buydowns, lender credits, HELOCs, and refinance break-even timing) so you can make a confident move.

Want a Personalized Rate Plan?

Choose the easiest next step:

Or call/text: (951) 760-8307 • Felicia Morales, Broker Owner (DRE 01471238 | NMLS 334006)

FAQ: Quick Answers I’m Getting This Week

Are rates going to drop more soon?

Rates can change daily. Next week’s Fed announcement and upcoming jobs data can move markets. I recommend watching trends, but locking based on your payment comfort and timeline.

Should I wait to buy until rates improve?

In many Temecula Valley pockets, the bigger factor is your overall monthly payment and purchase strategy (price, concessions, buydowns). Sometimes a good home + smart terms beats trying to time the bottom.

Do VA loans usually run lower than conventional?

Often yes, but not always. VA pricing can be excellent, especially with strong credit and the right lender. I’m happy to run a VA vs conventional comparison for your scenario.

Is a refinance worth it right now?

It depends on your current rate, loan size, and how long you’ll keep the home. I’ll calculate break-even and show you options (including lender credits and temporary buydowns where available).

Can I access equity without refinancing my first mortgage?

Yes - in many cases a HELOC or second lien can be a fit. We’ll look at goals (debt payoff, renovations, reserves) and the most cost-effective route.

Disclaimer: Rates shown are national averages for educational purposes and may not reflect your specific scenario. Actual terms vary by borrower qualifications and property details.