Blog > Best Month for Home Price Gains in Over a Year - But Context Matters

Best Month for Home Price Gains in Over a Year - But Context Matters

This week’s theme is context. Headlines can sound dramatic in either directio, but when you zoom out, the story usually becomes clearer (and more useful for real decisions).

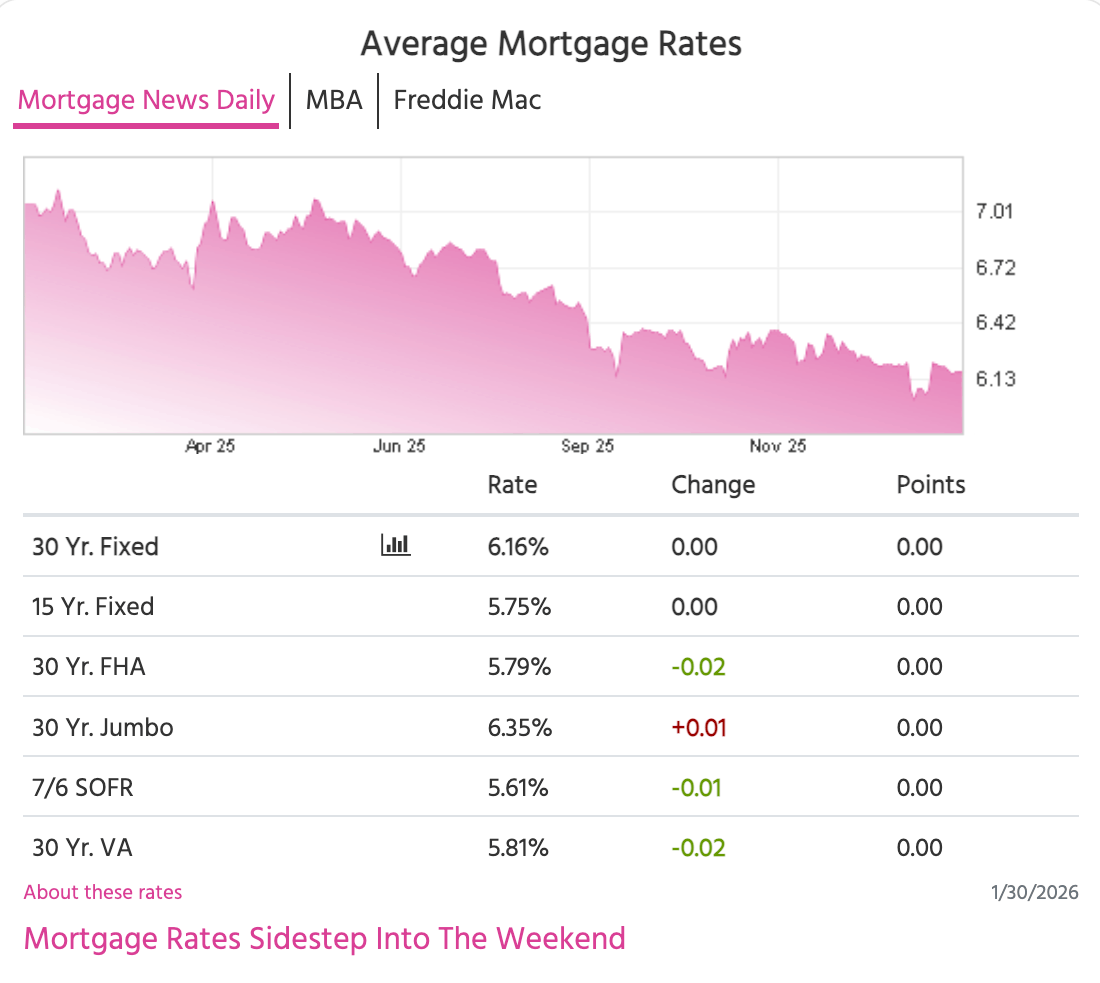

This Week’s Mortgage Rate Snapshot

Refi Activity Popped — But Zoom Out

Earlier this month’s rate rally created an obvious bump in refinance applications — and on the surface it looks like a mini boom. But when you compare it to historic refi waves, we’re still closer to historical lows than “boom times.”

Why? Most homeowners already have ultra-low rates from 2020–2021, so the biggest refi opportunities today tend to be for people who bought more recently (when rates were higher), or homeowners with a specific goal (cash-flow relief, debt consolidation, term change, or equity strategy).

Home Prices Had Their Best Monthly Gain in Over a Year

New housing data showed the fastest month-to-month home price appreciation in over a year - and yes, that sounds like a big deal. Here’s the “context” part:

- Seasonality matters: some months historically rise more than others.

- Timing matters: housing price data often lags. it doesn’t instantly reflect last week’s rate movement.

- Trend matters: year-over-year price growth is still positive, but it’s been running much slower than the last few years.

Bottom line: prices are still at all-time highs, they’re just not surging upward at the same pace.

What Rates Did This Week

The bond market looked choppy day-to-day, but in the bigger picture it was mostly a week of consolidation after the prior week’s bigger move. In other words: a lot of noise, without a major new direction.

What I’m Watching Next Week

Next week has a heavier lineup of reports that can move rates more meaningfully, including key manufacturing/services reports and jobs data. The biggest potential volatility usually comes from the monthly jobs report.

If you’re within a short window to buy or refinance, it’s smart to have a lock strategy, not just a “hope rates drop” strategy.

What This Means for Temecula Valley Buyers & Homeowners

- Buyers: When rates stabilize, competition can quietly heat up. The goal is the right payment + the right offer structure (credits, buydown options, and timelines).

- Homeowners: If refinancing doesn’t make sense, there may still be a smart equity plan (HELOC / second lien) depending on your goals.

- VA: If you’re VA-eligible, it’s always worth pricing both VA and conventional, sometimes the spread is meaningful.

Want a Personalized Rate Plan?

Choose the easiest next step:

Or call/text: (951) 760-8307 • Felicia Morales, Broker Owner (DRE 01471238 | NMLS 334006)

FAQ: The Quick Questions I’m Getting

Should I wait to buy until rates drop?

I focus on the full payment strategy: price, credits, buydown options, and timing. Sometimes the right home + smart terms beats trying to time the perfect week.

Is refinancing “back”?

Refi demand has improved, but it’s very scenario-specific. If you bought in the past few years, or you have a clear goal, it’s worth running numbers.

What if a refi doesn’t make sense?

We can look at equity access options like a HELOC/second lien - especially if the goal is renovations, debt cleanup, or reserves without touching your first mortgage.

Can you quote a rate from this blog?

These are averages. If you want accurate pricing, I’ll price it based on your scenario (loan type, credit, down payment, property, and timing).

Disclaimer: Rates shown are national averages for educational purposes and may not reflect your specific scenario. Actual terms vary by borrower qualifications and property details.