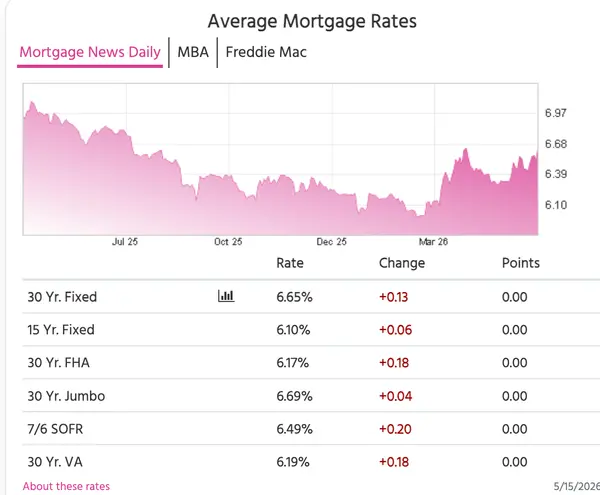

Mortgage Rates Climb to 9 Month Highs

Mortgage Rates Climb to 9 Month Highs Mortgage rates moved noticeably higher this week, reaching some of the highest levels we’ve seen in roughly nine months. After several weeks of volatility, the bond market faced renewed pressure from inflation concerns, global events, and rising Treasury yields,

Read More

Paseo del Sol Temecula: What to Know Before You Buy

Paseo del Sol Temecula: What to Know Before You Buy If you're searching for homes in Temecula and Paseo del Sol keeps coming up, there's a reason for that. It's one of the most established, well-rounded communities in South Temecula, and for buyers who want walkability, strong schools, and a neigh

Read More

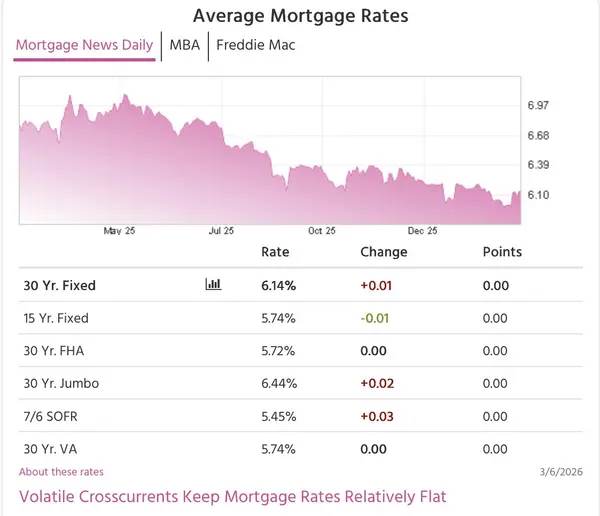

Mortgage Rates Pause After Volatile Stretch

Mortgage Rates Pause After Volatile Stretch If you’ve been watching mortgage rates over the past couple of weeks, you’ve probably felt how quickly things shifted. Rates moved sharply higher recently, one of the faster increases we’ve seen in a while, and then this week, instead of continuing that cl

Read More

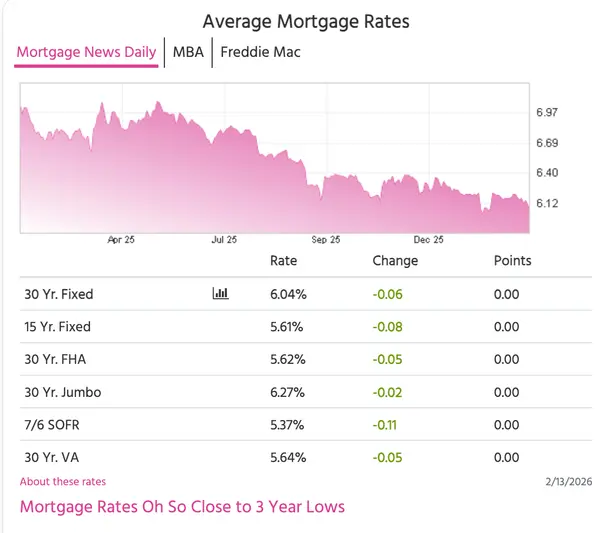

Mortgage Rates Jump to 7-Month Highs

Mortgage Rates Jump to 7-Month Highs Mortgage rates saw a noticeable move higher this week, reaching the highest levels in roughly seven months. While the jump happened fairly quickly, it’s important to remember that rate movement often happens in short bursts as financial markets react to global an

Read More

Recent Posts