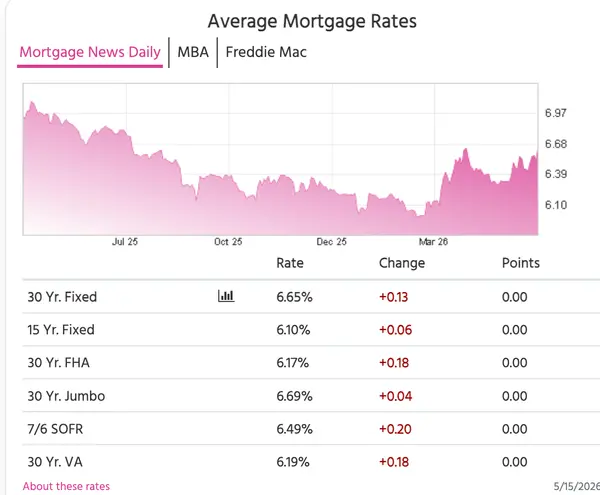

Mortgage Rates Jump to 7-Month Highs

Mortgage Rates Jump to 7-Month Highs Mortgage rates saw a noticeable move higher this week, reaching the highest levels in roughly seven months. While the jump happened fairly quickly, it’s important to remember that rate movement often happens in short bursts as financial markets react to global an

Read More

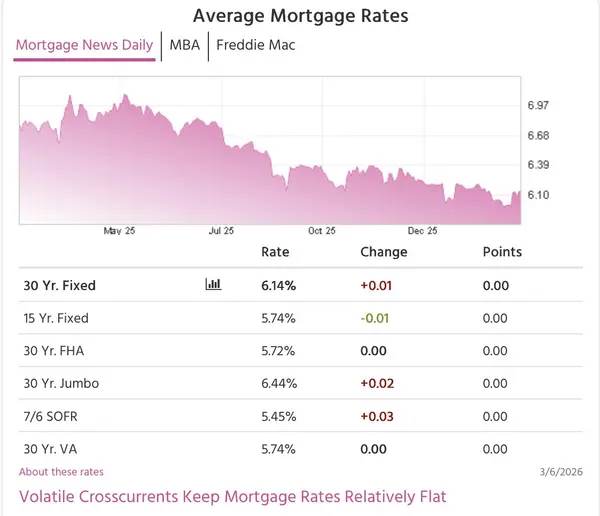

Mortgage Rates Rocked by Global Events This Week

Mortgage Rates Rocked by Global Events This Week Last week mortgage rates were sitting at multi-year lows and markets were unusually calm. This week was a different story. Rates moved higher and returned to levels seen earlier in February as global events added volatility to the bond market. Even

Read More

Temecula Valley Homes Under $400K: What’s Actually Available Right Now

Temecula Valley Homes Under $400K: What’s Actually Available Right Now If you’ve been wondering whether you can still buy in Temecula Valley under $400,000, the answer is yes — but it helps to be realistic about what that price point usually looks like. Most properties under $400K in Temecula Vall

Read More

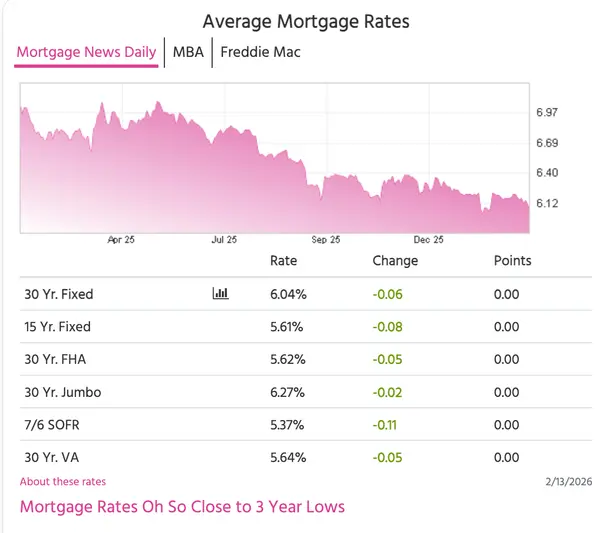

Rates Hit 3 Year Lows Despite Market Volatility

Rates Hit 3-Year Lows Despite Market Volatility This week was short (holiday week) and surprisingly calm overall in the bond market, even with a major headline that could have easily created bigger swings. The result: mortgage rates ended the week right in line with the lowest levels we’ve seen in

Read More

Recent Posts